How to think about the rising inflation and mortgage rates?

Disclaimer: This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for tax, legal, financial, or accounting advice. You should consult your own tax, legal, financial, and accounting advisors before engaging in any real estate transaction.

What does the 40-year high inflation rate of 8+% mean to a prospective home buyer in the Greater Seattle area? This is a multifaceted subject, and in this brief write up we will highlight how you should reason through the current environment.

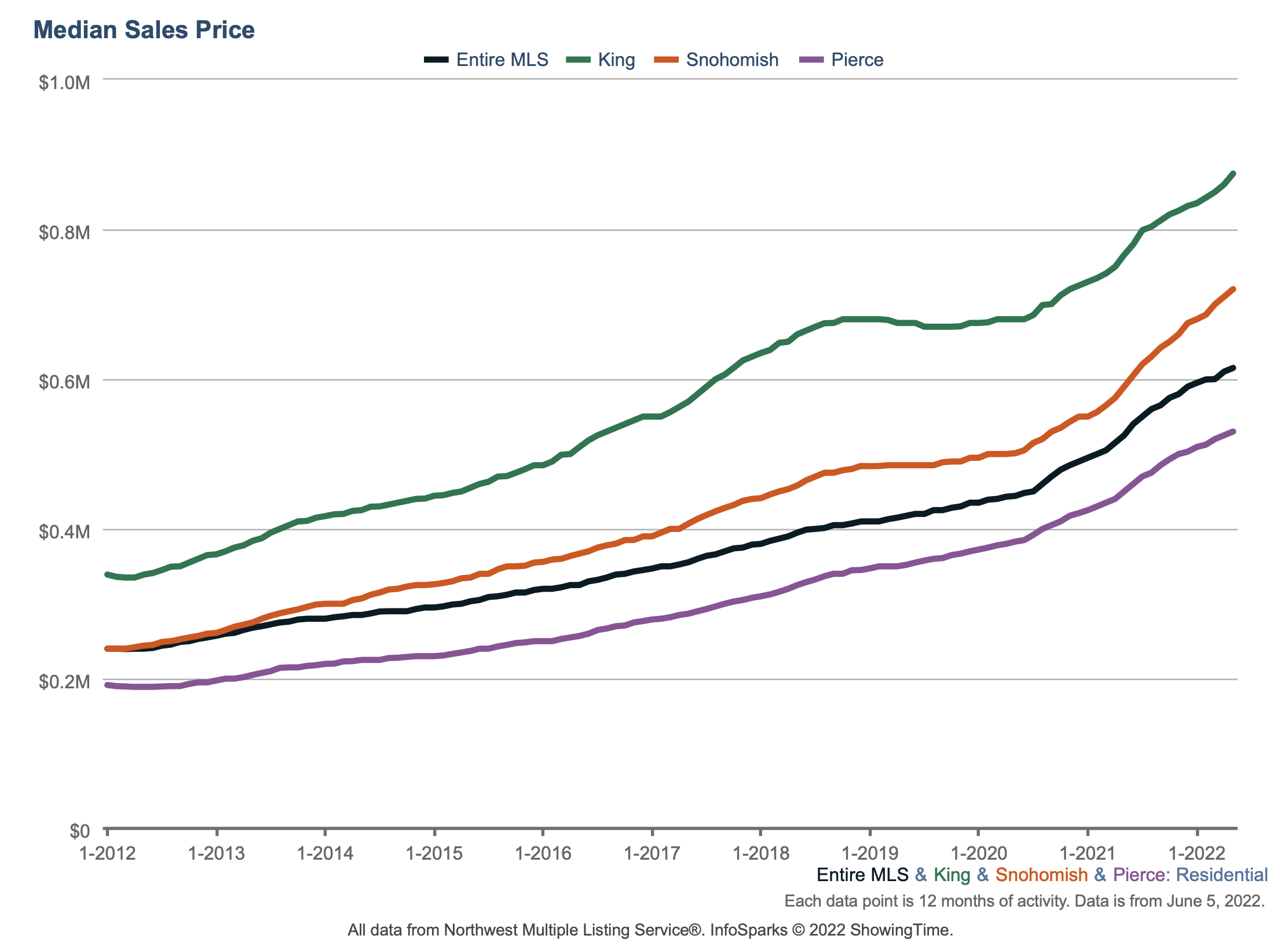

Rising home prices: The following figure shows the median home prices in King, Snohomish, and Pierce Counties as well as the entire Northwest Multiple Listing Service (NWMLS) from January 2021 till the end of May 2022. We can see clearly that prices continue to rise. This observation is consistent with the historical strength of real estate as an inflation hedge indicating that high inflation tends to boost home prices.

Rising interest rates: To get inflation under control through lowering the supply of money, the Federal Reserve has recently increased the benchmark rate and has signaled that more increases are likely to come. This, in turn, has increased mortgage interest rates. While a higher interest rate tends to lower the number of potential home buyers (hence lowering the demand), this is unlikely to make a fundamental dent in the home prices in the Greater Seattle area for two reasons:

Very low supply of real estate: The chronically low supply of homes in the Greater Seattle area is likely to counter the effect of any marginal decrease in demand on prices. As an example, a typical 3-bedroom home in King County has sold at or above the listing price over the past decade. In other words, the low supply of homes in the area can make multiple buyers compete over the same home. There have been numerous cases of multiple buyers trying to outbid each other to buy a listed home. Considering the tight home supply in the area (driven by the high cost of labor and materials as well as stringent regulations), it seems unlikely that a marginally lower demand (driven by the rising mortgage rates) could lower home prices in a substantial and sustainable manner.

Continued arrival of skilled professionals: The Greater Seattle area is home to headquarters and satellite offices of some of the world's leading companies. This factor continues to bring in highly in demand skilled (and typically well-paid) professionals. The influx of these professionals adds to the pool of qualified home buyers and helps sustain the upward pressure on real estate prices in the area.

Sentiments around the rising mortgage rates: Having a choice, nobody prefers to borrow at a higher interest rate. So if you don’t like the rising rates as a buyer, you’re not alone, and that feeling is completely natural. To make a good buying decision though, you need to think like a businessperson:

Mortgage interest rates are only meaningful in the context of the inflation rate: A high inflation rate diminishes the consumer’s buying power for food, rents, home, and everything in between faster. Therefore, you should think of mortgage interest rates not as absolute numbers but relative to the inflation rate. For example, with the inflation at a 40-year high of 8+%, if you borrow at 6% to buy a home and your home appreciates in value at an annual rate of 8+%, you’re doing a fantastic job of beating the inflation.

You’re not necessarily stuck with the interest rate you borrow at: You could (and probably should) refinance your loan in the future when the mortgage interest rates eventually fall. Refinancing your mortgage in the future can allow you to take advantage of better rates and, optionally, take cash out of the equity you build up by then (i.e., cash out refinance). In contrast, if you withhold from buying a home until rates come down (for example, in two years), you will be missing out on the appreciation gain of your home in the meantime – the cost of this missed opportunity can be hundreds of thousands of dollars.

Conclusion: While we cannot predict the future, our goal here is to share our insights driven by our real estate investing experience in the area, continued research, and interactions with clients and real estate professionals. Given the factors we laid out above, we are planning on buying more investment properties this year to add to our own investment portfolio. It’s one thing to tell others what to do with their money, and quite another to share with you what we’re actually doing with ours.

Your action items:

Let’s talk about your goals and come up with a plan tailored to your needs and aspirations. We will go through your goals, thoughts, concerns, and find the best path forward for you.

If you’re considering buying, get your mortgage rate locked as soon as you can. Once you lock the rate, you could go shopping knowing that any further interest rate increases, as signaled by the Federal Reserve, won’t affect your mortgage rate over the lock period. (Note that not all lenders offer rate locking. We’d be happy to refer you to lenders who do so.)