Market Update — April 2024

We firmly believe timely and relevant data is key to making good decisions. To this end, we are committed to providing our community and clients with actionable data and insights about the local real estate market.

Local real estate market

With the data from March 2024 in, here’s an overview of the key aspects of the local real estate market. The real estate data below is collected from Northwest Multiple Listing Service (NWMLS).

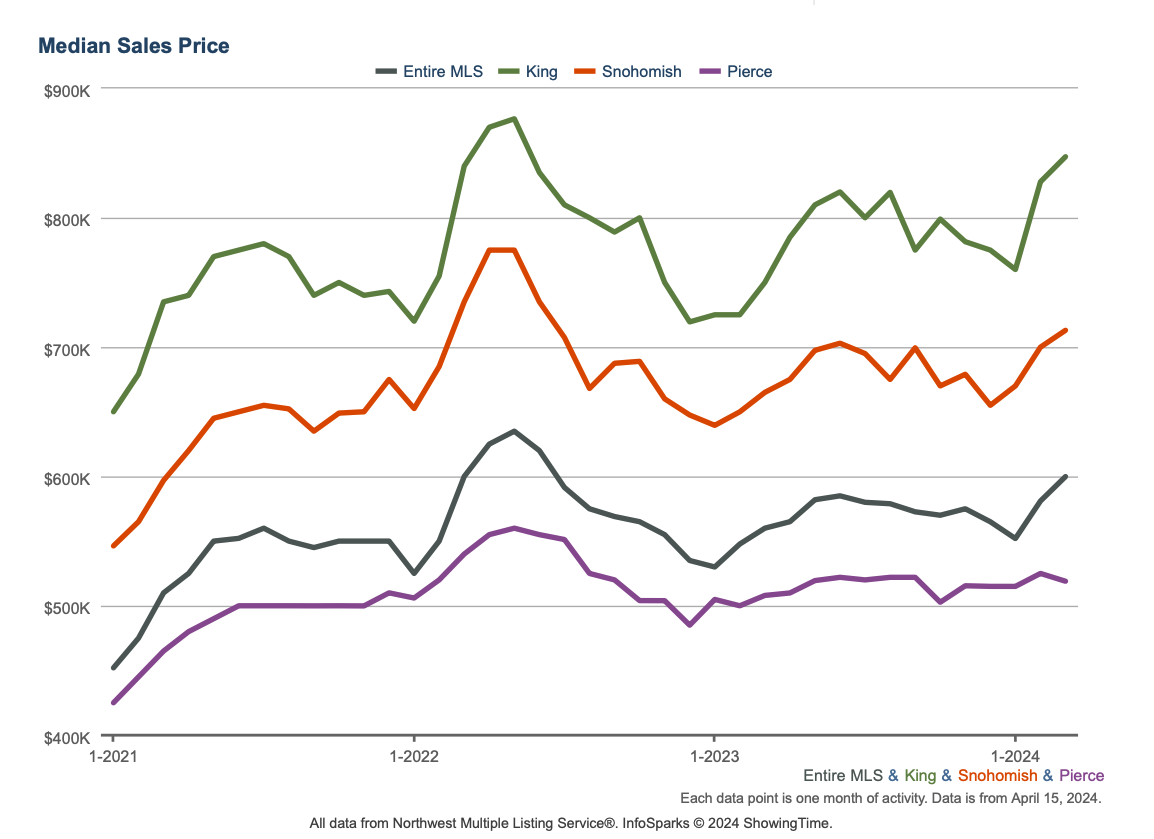

Median price: The chart below shows the latest median sales prices of homes over the past three years in the Greater Seattle area over the past three years:

Homes sold: 5,165 homes were sold in March 2024. The median price of $633,717 which represents a +7.4% growth YOY. This translates to a dollar value of about $4.1B.

New construction: 915 new construction homes were sold in March 2024. The median sale price of new construction homes was $739,000.

Months of inventory: Given the current quantity of supply, it’ll take around 1.6 months for every listed home to sell. To put this number in context, note that the months of inventory for a balanced market is considered to be 4 to 6 months. The four counties with the lowest months of inventory in March 2024 were were Snohomish (0.8), King (1.23), Pierce (1.39), and Kitsap (1.41). So the current data confirms the enduring shortage of supply relative to demand in the area.

New listings: 8,028 new listings were added to the NWMLS database in March 2024. This is an increase of 1.6% from March 2023.

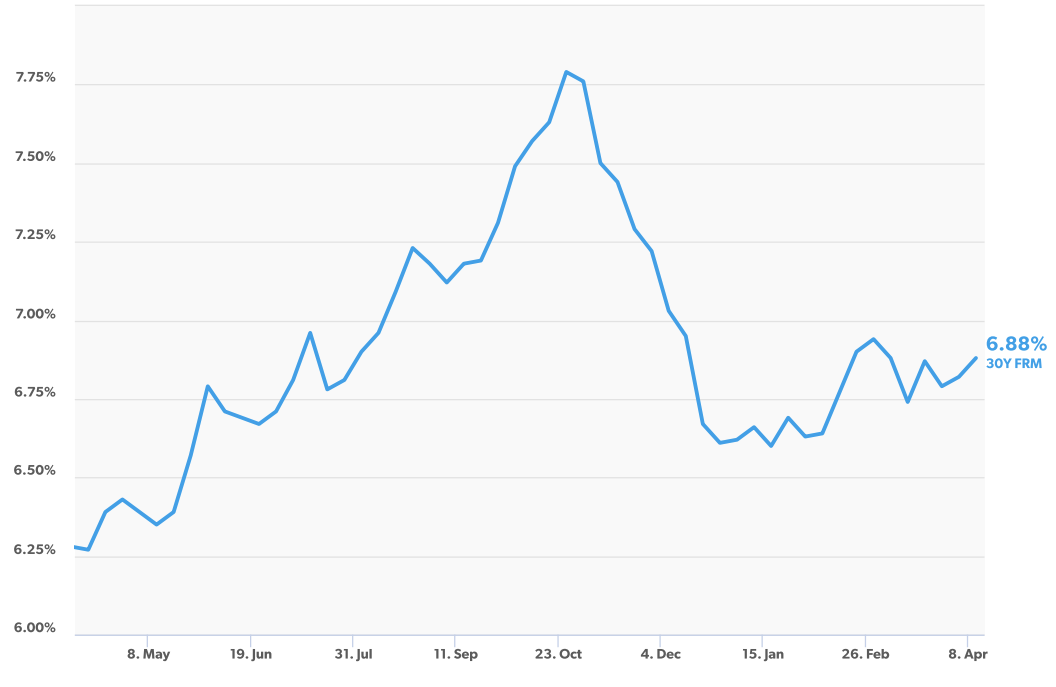

Mortgage rates: The Freddie Mac rate has edged and stayed down from it’s high in October/November 2023.

Average 30-Year Fixed Mortgage Rates over the past 12 months (Source: Freddie Mac)

Broader economy

Inflation progress stalls: The latest Consumer Price Index (CPI) showed higher than expected inflation in March, with the headline reading up 0.4% from February. On an annual basis, CPI moved in the wrong direction, rising from 3.2% to 3.5%. The Core measure, which strips out volatile food and energy prices, increased 0.4% while that annual reading remained at 3.8% (though it was expected to decline to 3.7%).

March Job Gains Roared in Above Estimates: The Bureau of Labor Statistics (BLS) reported that there were 303,000 jobs created in March, which was much stronger than expectations of 200,000 new jobs. Revisions to January and February added 22,000 jobs in those months combined. However, losses in full-time jobs were offset by gains among part-time workers and multiple job holders. The unemployment rate fell from 3.9% to 3.8%. It has remained in a narrow range between 3.7% and 3.9% since last August.